Follow the money in aviation technology this year and a clear picture emerges — plus a conspicuous blank space. The picture is a large, AI-heavy wave of spending aimed at the passenger. The blank space is the operational data layer underneath it, where the schedule actually lives. For anyone thinking about where durable value gets built, the blank space is worth a closer look.

The spend, sized

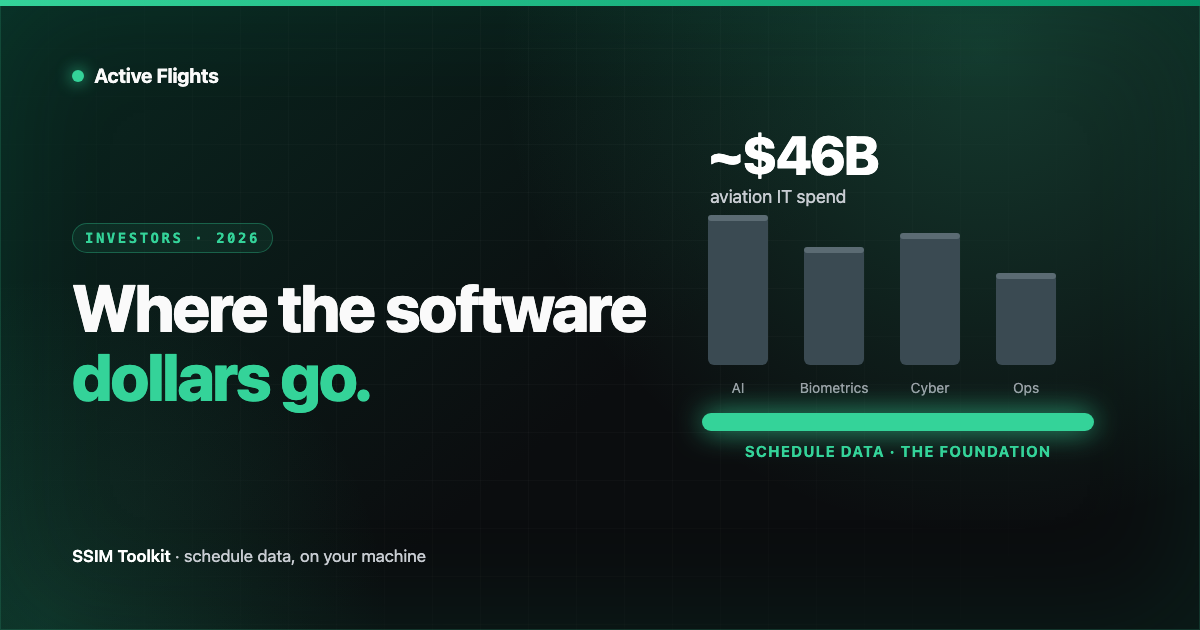

A few figures set the scale. Industry body SITA projects airlines and airports will spend on the order of $46 billion on IT across the near term — roughly $37 billion from airlines and $9 billion from airports. Broader market trackers put total IT spending in aviation around $29 billion in 2026, on a path toward the $60-billion range by the mid-2030s. The narrower aviation software market is smaller — estimated near $12 billion — but growing steadily.

(Worth a caveat: these are different scopes — total IT versus software-only versus airline-plus-airport — and independent researchers’ estimates vary widely. Treat them as order-of-magnitude, not gospel.)

| Aviation technology spend, 2026 (approx.) | Scope |

|---|---|

| ~$37B | Airline IT spend (SITA) |

| ~$9B | Airport IT spend (SITA) |

| ~$46B | Airline + airport IT, combined |

| ~$29B → ~$60B by mid-2030s | Total IT-in-aviation market (trackers) |

| ~$12B | Aviation software market (narrower) |

Where is it going? SITA’s read is unambiguous about the theme: 97% of airlines and 82% of airports report investing in AI, alongside a biometrically enabled passenger journey, data-driven operational efficiency, and sustainability. Security underpins it all — around 66% of airlines and 73% of airports name cybersecurity a top concern.

What that spend is (and isn’t) buying

Most of this capital is pointed at the experience and the perimeter: touchless check-in and boarding, biometric identity, disruption apps, loyalty, revenue and pricing intelligence, and the security to protect all of it. These are real priorities and mostly good investments.

Notice what’s not on the marquee: the boring, foundational schedule-data layer. The IATA SSIM feed — millions of fixed-width records exchanged between carriers, airports, GDSs, and coordinators — is the substrate every one of those flashier systems ultimately depends on. If the schedule is wrong, the biometric gate, the disruption app, and the revenue model are all reasoning about the wrong flights.

And yet this layer is, across much of the industry, still handled by in-house parsers and spreadsheets. It’s the classic pattern: a couple of engineers write the company’s fourth schedule parser, it’s fast for some carriers and brittle on others, and the bill compounds every year in maintenance and missed edge cases. Almost none of that $46 billion is aimed at fixing it, because it isn’t the part anyone demos.

The most-funded layer in aviation software is the one the passenger sees. The least-funded is the one everything else is built on.

The investor-shaped gap

Under-tooled, universally needed infrastructure is exactly the kind of gap that tends to reward a focused product. A few reasons this one looks structurally attractive:

- It’s a genuine standard. SSIM isn’t a fad format; it’s how the industry has exchanged schedules for decades and will for decades more. Tooling built on a stable standard doesn’t churn with fashion.

- The pain is recurring, not one-off. As the last two years have shown — record load factors, a multi-year aircraft backlog — schedules are rewritten continuously. The need to read, validate, compare, and deconflict them is permanent.

- Build-vs-buy is tilting. Every team maintaining a home-grown parser is paying an invisible tax. When a dependable tool exists, “why are we still maintaining this?” becomes an easy question to answer.

- AI raises the stakes on data quality, not lowers them. The more decisions get automated on top of the schedule, the more it matters that the schedule underneath is correct and reproducible.

That last point deserves emphasis, because it’s where a lot of aviation-AI enthusiasm gets the architecture backwards.

AI on the outside, determinism on the inside

The instinct in a 97%-investing-in-AI market is to put a model at the centre of everything. For schedule data, that’s the wrong place for it. You do not want a model guessing how many flights operate on a Tuesday or which aircraft flies a rotation — you want those answers derived deterministically from the spec, the same way every time, so they’re auditable and reproducible.

The right shape is AI on the outside of a deterministic core: let an analyst point their own AI assistant at a schedule to explain a validation warning, summarise a diff, or draft a query — while the engine that computes the numbers stays boringly, verifiably exact. That’s the design we favour: a read-only, on-device integration that lets an assistant explore the data without ever being the thing that decides the numbers. AI as an interface, not as the source of truth.

The takeaway

The 2026 spending wave is aimed, sensibly, at the passenger and the perimeter. But the schedule-data foundation that all of it rests on remains largely unbought — still stitched together in-house, still a recurring tax, still under-invested precisely because it isn’t the shiny part. For operators, closing that gap is an efficiency and resilience play. For investors, an under-tooled layer sitting beneath a $40-billion-plus spend, built on a durable standard with permanent demand, is the kind of quiet opportunity that tends to age well.

It’s the layer we’ve chosen to build for — deliberately foundation-first, local, and deterministic. The flashier systems can sit on top; they’ll all be better for standing on schedule data they can trust.

Spend and adoption figures are from SITA’s air-transport IT research and third-party market trackers cited below. Scopes and methodologies differ; figures are approximate.

Sources

Want early access?

We're opening SSIM Toolkit to teams in waves through 2026 — free during the preview. Drop your email and we'll reach out when it's your turn.

You're on the list.Check your inbox for a confirmation email to finish signing up.

Something went wrong — please try again, or emailhello@activeflights.com.