Decarbonisation is usually filed under “sustainability.” In 2026 it’s increasingly an operations and economics story too — because Europe’s ReFuelEU Aviation mandate, the price of sustainable aviation fuel, and where that fuel is actually available are starting to shape how and where airlines fly.

The mandate, the price, the supply

Three facts set the scene:

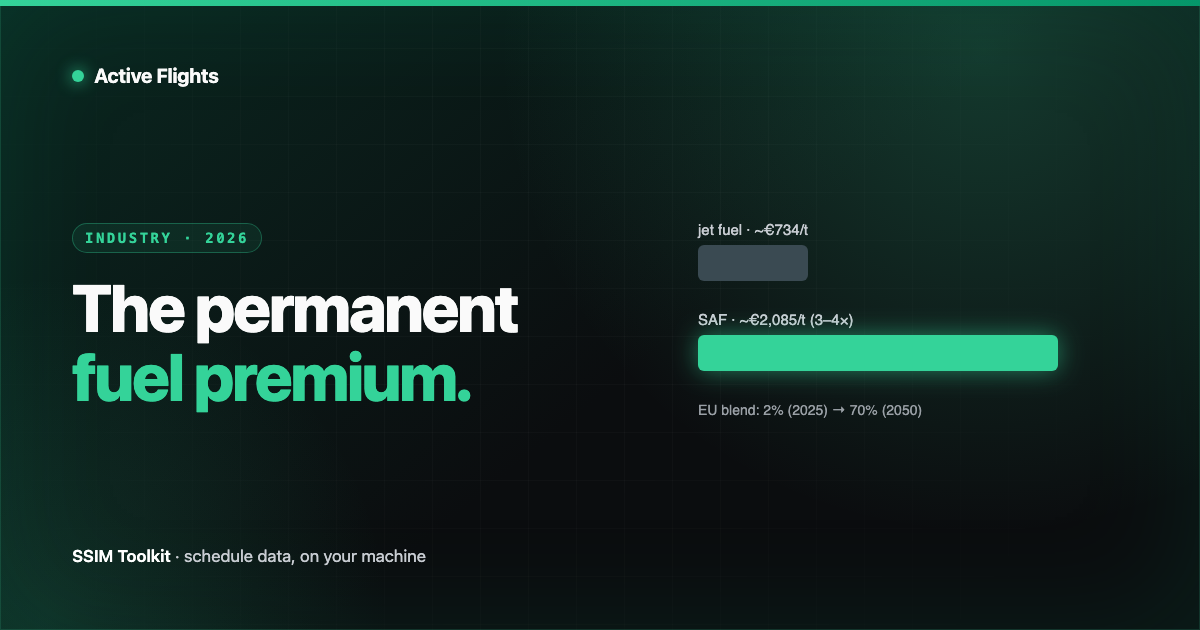

- The mandate ramps. ReFuelEU requires fuel suppliers at EU airports to blend a rising share of Sustainable Aviation Fuel (SAF) — 2% from 2025, climbing to 70% by 2050. Switzerland adopted the same regime at Zurich and Geneva from January 2026.

- The premium is steep — and looks permanent. SAF has run around €2,085 per tonne versus roughly €734 for conventional jet fuel (EASA figures) — three to four times the price. Analysts increasingly treat that premium as structural, not transitional.

- Supply is thin and concentrated. Global SAF output is projected around 2.4 million tonnes in 2026 — about 0.8% of jet-fuel use, with consistent availability at only a handful of airports (Amsterdam, Copenhagen, Oslo, London, Los Angeles, San Francisco).

To push things along, eight member states formed an e-SAF Early Movers Coalition, committing €500 million toward a pilot tender later in 2026.

Airlines from Ryanair and Wizz Air to easyJet and Lufthansa are already reworking cost structures around these rules; when a core input triples in price on part of your network, it doesn’t stay a footnote.

Why this reaches the schedule

A price premium that varies by airport and by fuel availability turns fuel into something that looks a lot like the other constraints we’ve written about (slots, MCT): a dataset that has to be applied against the schedule to make good decisions.

- Tankering vs compliance. Where SAF is scarce or expensive, carriers weigh carrying extra conventional fuel from cheaper stations against mandate and weight penalties — a routing-and-schedule question, not just a fuel-desk one.

- Airport-level economics. The cost of operating a given rotation now depends on which airports it touches and what fuel regime applies there. That’s schedule data meeting reference data, again.

- Network nudges. Over time, structural fuel-cost differences feed back into which frequencies and markets pencil out — the slow kind of pressure that reshapes a schedule season over season.

Decarbonisation policy is becoming an input to the schedule — one more airport-keyed dataset that has to line up with the flights you actually plan to fly.

The takeaway

SAF is the right direction and a hard one: supply is tiny, the premium is real, and the rules are ramping regardless. For schedule teams, the lesson is familiar — another external dataset, keyed by airport, that has to be held against the schedule to reason correctly about cost and compliance. The airlines that manage it well will be the ones whose schedule data and reference data actually talk to each other.

Sources

Want early access?

We're opening SSIM Toolkit to teams in waves through 2026 — free during the preview. Drop your email and we'll reach out when it's your turn.

You're on the list.Check your inbox for a confirmation email to finish signing up.

Something went wrong — please try again, or emailhello@activeflights.com.